A Simple Model of Housing Prices

A Simple Model of Housing Prices

Trying to change Scott Alexander's mind about housing

Recently Scott Alexander published a text saying he thought more housing would lead to higher housing prices due to agglomeration effects, using as evidence the correlation between prices and density in the US, and asked us to change his mind about housing. Here’s my shot at it.

Note: In this posts all references to “rent” mean economic rent, not the price of housing.

A Simple Model of Housing Prices

In a world where land does not matter, let’s say people have tech to build infinitely high buildings and a teleporting elevator, housing prices will be just the construction costs. The supply curve of housing will be infinitely elastic, no matter how many people want to live somewhere, if they’re willing to pay the costs of building a new floor they get it at that price.

In this world people everywhere pay the same price for housing, no matter if they live in a big city or in the middle of nowhere. Places becoming more desirable lead to more people there and no increase in prices. Also note that in this place there’s only consumer surplus.

Lets imagine someone places a ban on building higher than X floors, and we’re in an island with only space for one building. Now the supply curve is infinitely elastic under some quantity supplied, and infinitely inelastic above it.

Now increases in demand lead to quantity increases and no price increases up to some point, and after that all shifts upward in demand lead to no quantity increases and price increases.

Also as soon as the quantity supplied gets to the supply curve limit, consumer surplus gets to a maximum, and after that all shifts upward in demand will lead to a increase in producer surplus only. This will take the form of land rents.

Of course nowhere is like this.

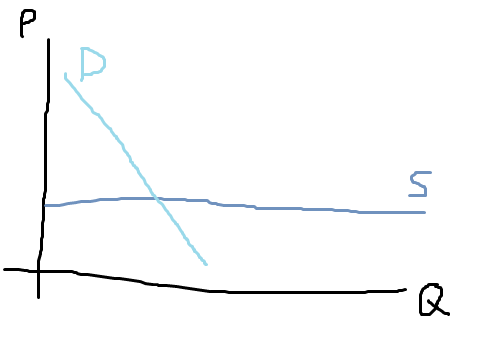

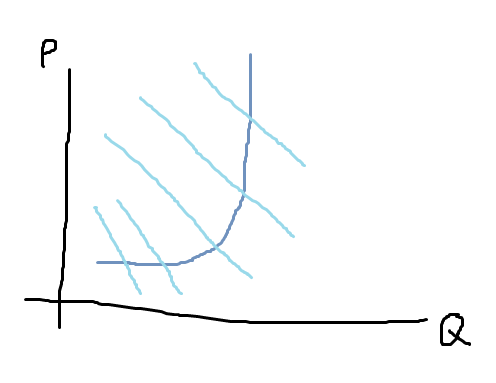

A just a tiny bit more realistic simple model of housing

So imagine a different world now, people can’t stack buildings infinitely, so buildings can get a little bit more expensive for each floor you add. Also people will start complaining about building and put regulations in place to constrain supply. More dense places will have stronger constrains, as there are more locals close by to any added housing to complain. This will lead to a supply curve that gradually gets more inelastic as quantity supplied goes up.

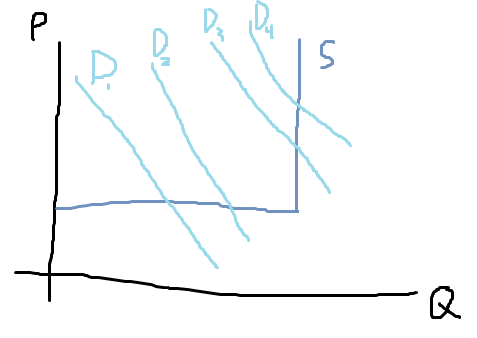

Pretty similar to the second unrealistic model. If we have lots of markets with a similar supply curve, but different demand curves we will get:

If you compare different places, places with high quantity supply will also have higher prices, but in each particular place, easing the supply constrains will lead to both more quantity supplied and lower prices

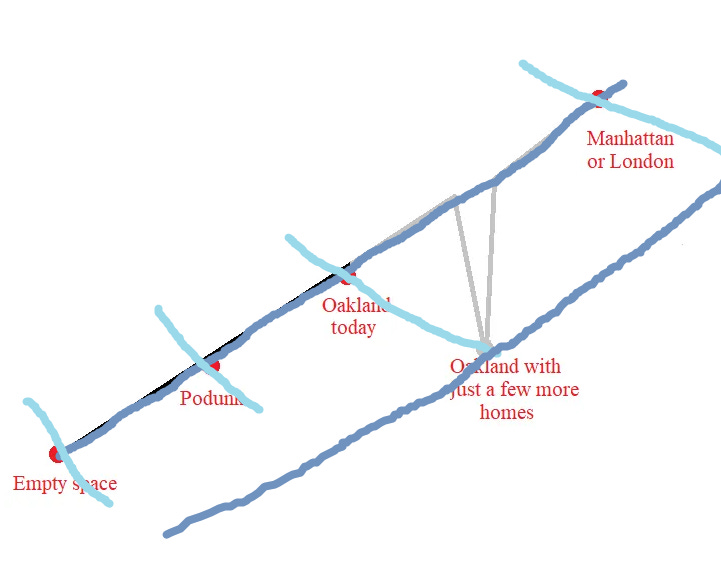

Which funnily enough reminds me of an image in Scott’s post:

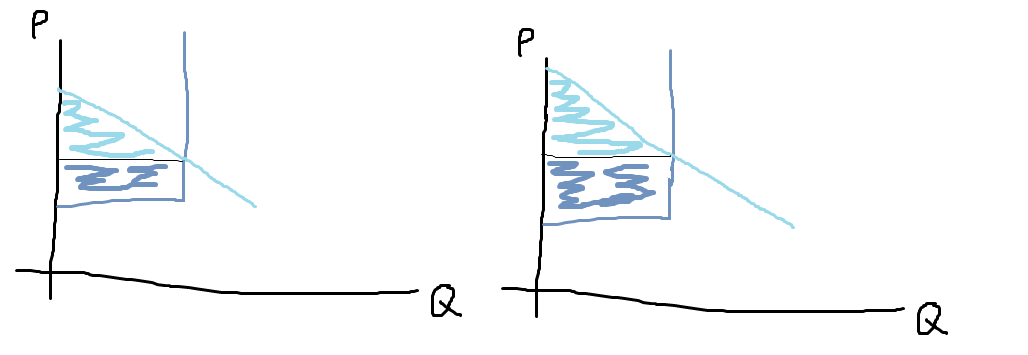

How does this model would look in real life

Now that we have a little model we should probably look at it’s predictions. Places with a higher quantity supplied in an inelastic regime would have higher prices, higher land rents, and less consumer surplus. The building that happens in these places is going up the supply curve because of higher demand, so it would be associated with prices going higher. Given that demand will be going up by a combination of population and GDP per capita growth, these places will have constantly rising prices, with growing land rents, and prices will rise more sharply in the places with a more restrictive regime, and more populated places, with associated small increase in quantity.

At the same time, lots of small places or places with more elastic supply would have low prices, low rents and would be responding to higher demand with more quantity increases than price increases.

Quantity supplied vs Supply

I think at the heart of the matter there’s some confusion in definitions of supply, Scott says:

The two densest US cities, ie the cities with the greatest housing supply per square kilometer, are New York City and San Francisco. These are also the 1st and 3rd most expensive cities in the US.

The thing is quantity supplied does not equal supply; supply is a function that links quantity and price. There’s no reason to think a place with more quantity supplied has a higher supply of a good. As an example, we have less horses today than in the past, but through cheaper food, better medicine, better breeding, etc we can supply any quantity of horses cheaper than we could in the past.

When people talk about housing policy, they are usually trying to get a better function that ties quantity and prices, not just change quantity supplied.

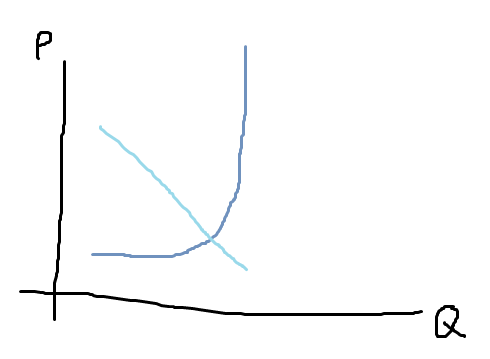

Scott’s agglomeration-demand slopping up model

Scott’s text implies a different model where demand slopes up, as the more quantity demanded the more people are willing to pay, until a certain point.

So if Oakland became bigger, it would become a more appealing destination for these people at some rate (making it more expensive) and get more supply at some rate (making it less expensive). Since existing big dense cities are all very expensive, most likely in current conditions the first effect would win out, and Oakland would become more expensive. But it can’t do this forever - at some point, it will exhaust the pool of Americans who want to move to big cities (you’ll know this has happened when housing prices are no higher in big cities than anywhere else). So there’s not perpetual motion - just the ability to keep making money as long as there’s pent-up demand, like in every other part of the economy.

What this would look like?

I’ll ignore the problems with multiple equilibria, etc.

What is Scott is proposing is that the correlation between price and quantity is driven by different supplies in different cities riding an upward sloped demand curve.

So cities are small because is expensive to build in them, and as it gets cheaper to build, more people move to the cities, making prices go up. Prices and land rents will be higher in places with less inelastic supply where is easier to build, and also be higher in places with more quantity supplied. This will happen only in a part of the curve, and if supply gets elastic enough we’ll go to the downward slopping part of the demand curve, where things are like the previous model.

Note that assuming people were once in the normal part of the curve, in some transitional moment highly restricting the supply lead to falling prices.

So which one is correct?

Both models predict a correlation between prices and quantities, but in one we have the places with higher prices and rent being the ones where is easier to build, where places that are adding the most units is where the price is rising the most, where in the past a big supply restriction lead to falling prices. In the other we have places with higher prices and rent being the ones where is hard to build, where places that are adding the fewer units are the ones where the price is rising the most, and where prices are steadily going up, and going up more in more restrictive places.

I’ll let you guys check the data.

PS: I highly recommend Kevin Erdmman’s substack and his book Shut Out about housing issues.